Connecting Back to Markets – Insights from the Smallholder Farmer Outcome Harvesting Survey of February 2025

Connecting Back to Markets – Insights from the Smallholder Farmer Outcome Harvesting Survey of February 2025

Our latest outcome harvesting survey conducted in February 2025 examined the interactions of smallholder farmers (SHFs) with services provided through the Climate Smart Jobs (CSJ) project, specifically component 1. The survey assessed how effectively SHFs were implementing climate-smart practices and whether these practices contributed to rising incomes and enhanced resilience to climate change over the long term. This summary outlines the essential findings and insights that can guide future investments and interventions by the private sector.

CSJ’s outcome harvesting survey is a crucial feedback mechanism that helps build evidence and insight into the effectiveness of its market-based interventions. By reconnecting with smallholder farmers (SHFs) after each farming season, the survey captures the changing experiences of individuals in the field, tracks the adoption of products and services provided by market actors, and assesses whether these changes result in meaningful improvements in household well-being. This blog presents the preliminary results following nearly a year of implementation (January-December 2024), providing a glimpse into the progress made and the insights gained for the project and its collaborators. It also lays the groundwork for upcoming surveys that will enhance our understanding of how the inclusive delivery of agricultural products and services can strengthen the resilience of SHF households against climate change, particularly in the unpredictable agricultural contexts found in Northern Uganda.

In ongoing discussions that take place after surveys are completed, the true nature of our impact becomes clear. During a conversation with a smallholder farmer, I was reminded of a crucial element: the necessity of transparency and feedback.

“How will I learn about the survey results?” I could sense both curiosity and caution in their inquiry—a sentiment that should not be ignored. It’s not just about providing feedback; it’s equally important to ensure that we promote inclusion and transparency. This underscores the idea that our engagement necessitates a commitment to follow-up.

“I last saw you during the training; what has transpired since then?” This question pointed to a deficiency in follow-up and continuity within our communication. We need to reflect on how our presence might be interpreted as a commitment. If we disappear without adequate explanation, we risk creating uncertainty among farmers and clients.

What did I learn from this interaction? I came to understand that the value of outcome harvesting lies not only in the metrics we gather but also in the insights we derive, especially from inquiries that may not have straightforward answers. This reflection acts as a quiet commitment to enhance our practices, to close the feedback loop, and to listen more carefully beyond the confines of the survey forms.

As at March 2025, Our collaboration with 40 private sector partners has generated some impact, we have mobilised over GBP 1.4 million in investments toward climate-smart agriculture investments in Northern Uganda. Through our technical assistance, 449 individuals have been supported and reached over 186,000 people with practical climate resilience information. As a result, partners have recorded GBP 1.6 million in additional sales. More than 23,000 smallholder farmers now access improved agricultural services, over 19,000 of whom are adopting climate-smart practices. In addition, our initiatives have contributed to the creation of over 180 full-time jobs.

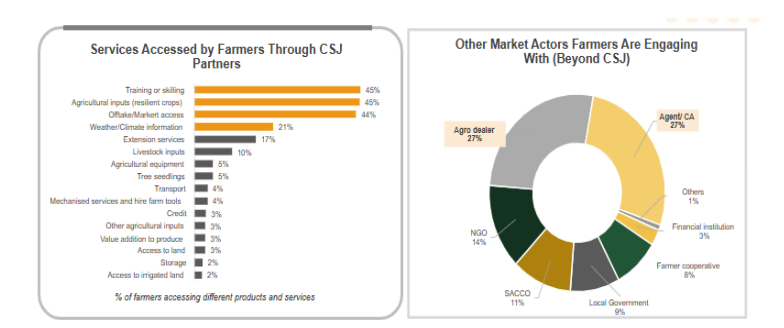

Market Interactions and Service Access: Among the 530 farmers surveyed, 93% reported accessing services or products, engaging with an average of three different market actors. Among those that accessed services/ products, the most utilised were training (45%), resilient inputs (45%), and offtake support (44%). In contrast, Credit and financial services were the least accessed, highlighting a persistent barrier to scaling interventions. Notably, female farmers accessed a broader range of services than their male counterparts, reflecting their increasing involvement in production activities.

Surveyed farmers are engaging directly with other actors in the agricultural value chain, with Agro-dealers and Commercial Agents the primary intermediaries between farmers and companies

First-Time Service Usage: Nearly half of the respondents accessed at least one service for the first time, indicating strong initial demand and satisfaction, particularly for female SHFs and refugees. Suggesting the relevance of promoted services and products

Adoption of Climate-Smart Practices: Climate-resilient seeds (52%), pest control (36%), and diversification (31%) were the leading practices adopted. However, there was a slower uptake of mechanisation technologies like threshers and tractors. On average, farmers adopted 2.4 practices, showing potential for scaling private sector solutions. Improved seeds were the most used input, suggesting a potential bundling opportunity with other services. However, some farmers expressed concerns about the efficacy, cost, and susceptibility of improved seeds to pests and diseases.

Household Dynamics and Decision Making: While most households are male-headed, decision-making is often shared, especially in agricultural activities. Women are slightly more likely to make decisions on what inputs to use, suggesting an expanding role of women in agricultural activities and decision-making.

Farmers’ spending patterns vary significantly between seasons. Season A sees higher costs for seeds and land preparation compared to Season B, except in the West Nile region, implying that seasonal timing influences how and when farmers invest in inputs. This variation is important for stakeholders offering financing or support. Notably, maize and soybeans incur nearly double the post-harvest costs in Season A compared to Season B.

Resilience: Farmers reported frequent shocks, particularly drought, dry spells, and pests. These shocks drive risk aversion, but they also reveal opportunities for adaptive products and services. Coping mechanisms are often limited: some 42% of farmers took no action to respond to adverse events, highlighting both gaps in preparedness and potential barriers to effective risk mitigation. Women farmers in Uganda face unique challenges. Nearly two-thirds of the farmers who reported doing nothing in response to adverse events were women. Negative net income was observed for several months, particularly affecting women and refugee households, thus limiting investments in climate-smart practices.

The findings from this outcome harvesting exercise offer valuable insights for private sector players to effectively navigate the evolving landscape in agriculture.

A persistent challenge is the inconsistency in record-keeping. Enhancing database systems is essential for improving operational efficiency and fostering a more effective feedback loop between agribusinesses and research efforts. Regular updates and verification of farmer information will enable businesses to engage in more targeted outreach and better understand shifting market requirements.

The traditional belief that men are the primary decision-makers within households is increasingly being challenged. Data from surveys shows that household decisions are frequently made collaboratively by both partners. Agribusiness marketing, product development, and service delivery should reflect this reality to ensure more inclusive outreach.

The growing influence of women in key areas, such as financial decision-making and household purchasing, presents a significant opportunity for businesses to develop products and services that cater to women's needs and preferences, acknowledging their vital role in managing homes and farms.

While control groups are ideal for comprehensive evaluations, their associated costs and logistical challenges can hinder market system development projects. Therefore, private sector stakeholders should support CSJ’s baseline studies conducted before onboarding and facilitate ongoing data collection to monitor progress and adapt strategies in real time.

Innovations should focus on enhancing household economies and contributing to the broader effort of building climate resilience. Achieving climate resilience necessitates a multifaceted approach that encompasses on-farm, off-farm, and non-farm activities. Relying solely on family labour can limit the scale and efficiency of agricultural operations.

So far, the implementation process has revealed both promising progress and persistent challenges in bolstering climate resilience and enhancing market engagement among smallholder farmers (SHFs) in Northern Uganda. The adoption of climate-smart practices, increased collaboration with the private sector, and substantial investment flows indicate significant advancements. Nonetheless, the issues raised by SHFs and the gaps they identify highlight that achieving a meaningful impact requires a continuous presence, effective communication, and flexible responses to evolving needs. As we look ahead to future surveys and further collaboration with private sector partners, our emphasis should be on boosting farmer inclusion, broadening successful interventions, and addressing the systemic barriers that impede resilience. Only through sustained efforts can we guarantee that market-driven solutions result in impactful, transformative changes for farming communities grappling with an increasingly unpredictable climate.

Our research underscores the importance of tailored interventions that consider regional disparities, gender dynamics, and the diverse needs of SHFs. Innovations should focus on strengthening household economies and supporting the ongoing initiatives to enhance climate resilience. By leveraging these insights, the private sector can foster mutually beneficial outcomes for both SHFs and market participants, thereby encouraging sustainable agricultural development.